What happens when lenders see a blank file

For many drivers and gig workers, an empty credit file means slow or no access to financing. That barrier is pragmatic: traditional banks rely on credit scoring and historical repayment data. DiDi recognized that constraint and built product pathways to onboard users without classic files — see didi finanzas for the platform approach. The user-centric model focuses on transactional signals instead of legacy scores, enabling didi prestamos via crédito revolvente that adapts as you build a track record.

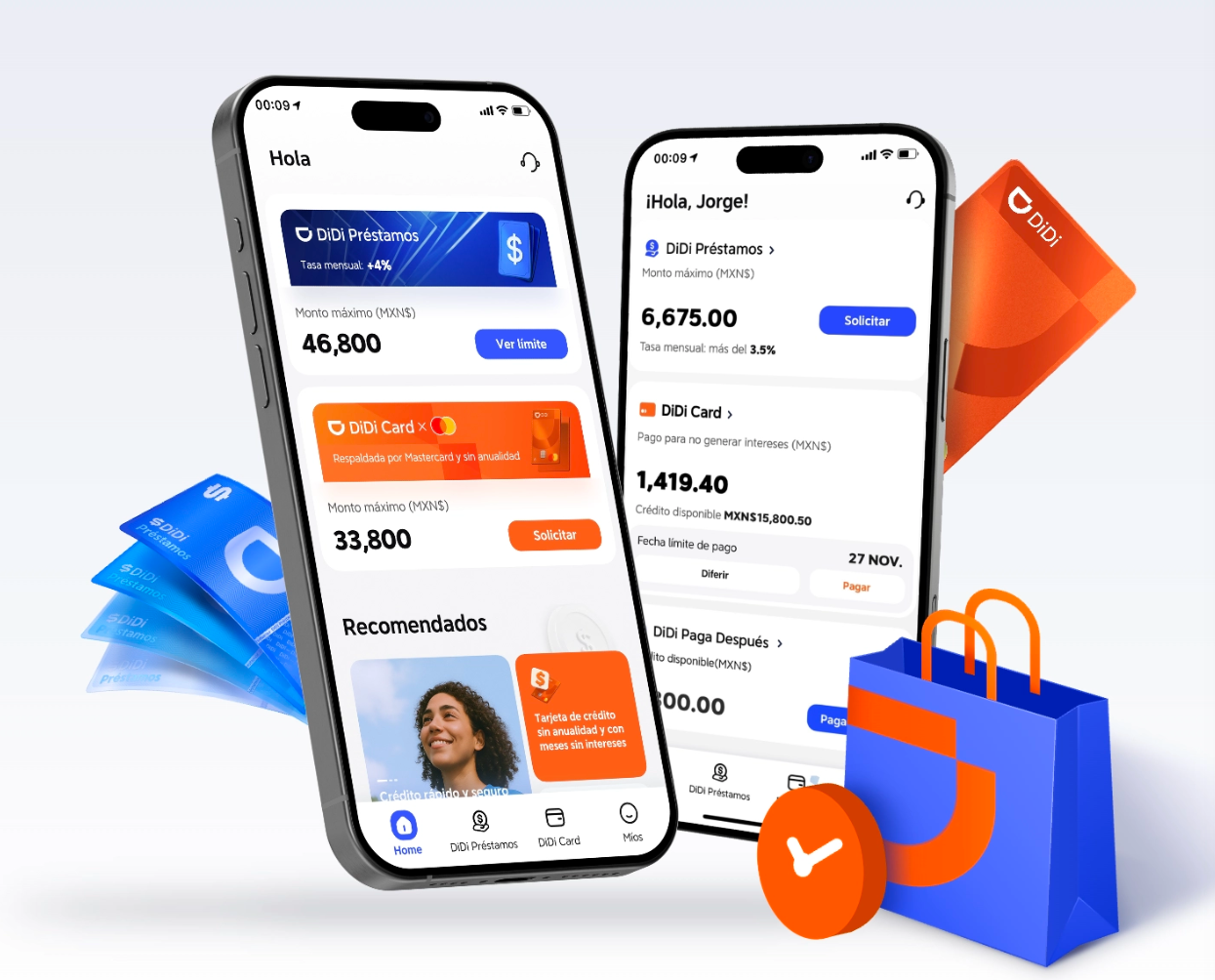

How the revolving-credit flow works in practice

Entry is lean: a lightweight KYC flow, permissioned data from ride activity, and a compact underwriting engine. That underwriting layer uses alternative data (trip volumes, acceptance rate, on-time completions) combined with a risk model to set an initial credit line. Credit revolvente means the line replenishes as you repay — practical for drivers whose income is pulsed. The system avoids heavy-weight documentation while keeping compliance tight through targeted API integrations with platform telemetry and payment rails.

User benefits and operational specifics

Users get three immediate wins: rapid access to working capital, flexibility to borrow as needed, and a clear repayment cadence tied to earnings. Operationally, DiDi applies soft checks first, then escalates to deeper verification as the line grows. This staged approach reduces friction while preserving controls on fraud and default. The product surface includes mobile in-app disbursement, scheduled payments synced to payouts, and transparent fee schedules so drivers can model cashflow accurately.

Common onboarding mistakes to avoid

Two missteps recur: over-borrowing against an early, small line; and missing scheduled repayments because cashflow timing wasn’t aligned. Avoid both by calibrating draw frequency and using auto-pay when possible. Also, treat small on-time payments as strategic — they help expand your line under DiDi’s credit revolvente mechanics. Little wins in repayment behavior compound into measurable line increases over months.

Comparatives and available alternatives

Competing fintech offerings may provide point loans or merchant cash advances; DiDi’s revolving credit differentiates by tying credit to activity telemetry and offering reuse without repeated applications. Traditional banks still win on interest rates for prime borrowers, but they lose on speed and accessibility for first-time applicants. For those who can wait and document income formally, a bank product could be cheaper — but for immediacy and operational fit with ride income, the revolving model is generally superior.

Trust, transparency, and real-world validation

Trust is earned through clear contracts and measurable outcomes. In Mexico City, where many gig workers lack traditional banking histories and World Bank reporting highlights significant unbanked populations in parts of Latin America, practical financial rails tied to platform income make a difference. DiDi’s public materials and product controls aim to address that — and if you’re weighing whether didi finanzas es confiable the evidence lies in repeat usage and line growth observed across cohorts. The mechanics are auditable: fee schedules, dispute paths, and repayment records are all available in-app.

How to evaluate if this fits your situation

Measure three things before committing: your typical weekly net after platform fees, the volatility of your trip volume, and the effective APR once fees are annualized. Align draw amounts to low-volatility weeks to avoid stress. Use the initial months to demonstrate repayment discipline — the system rewards consistent behavior with line increases and lower risk flags. A small disciplined line repaid on time is better than a larger line that creates liquidity strain.

Quick recap and actionable next steps

DiDi’s revolving credit model translates platform activity into a usable credit line without legacy score dependence. Start small, prioritize on-time repayments, and leverage in-app visibility to plan draws against expected payouts. – Track your draws versus net earnings weekly to avoid mismatch. These practical steps minimize cost and maximize access as your credit profile builds.

Golden rules for choosing and using platform credit

1) Liquidity-fit: Only borrow amounts that won’t exceed two weeks of core earnings in the worst week. 2) Cost transparency: Convert all fees to an annualized rate and compare to peers. 3) Behavioral leverage: Treat early repayments as an investment in higher future lines. Follow these metrics and you’ll make financing work for operations, not against them.

DiDi Finanzas — the product becomes the practical bridge between no-file status and ongoing access to capital; use it deliberately, and it scales with your work. –

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}